HDFC Bank Millennia and HDFC Bank MoneyBack+ are both entry-level HDFC credit cards designed for everyday spending, but they work differently. Both offer strong cashback rewards, making them top cashback credit cards in India for beginners. This comparison breaks down HDFC Bank Millennia vs HDFC Bank MoneyBack+ to help you choose based on your shopping habits.

Comparative Overview: HDFC Bank Millennia vs HDFC Bank MoneyBack+

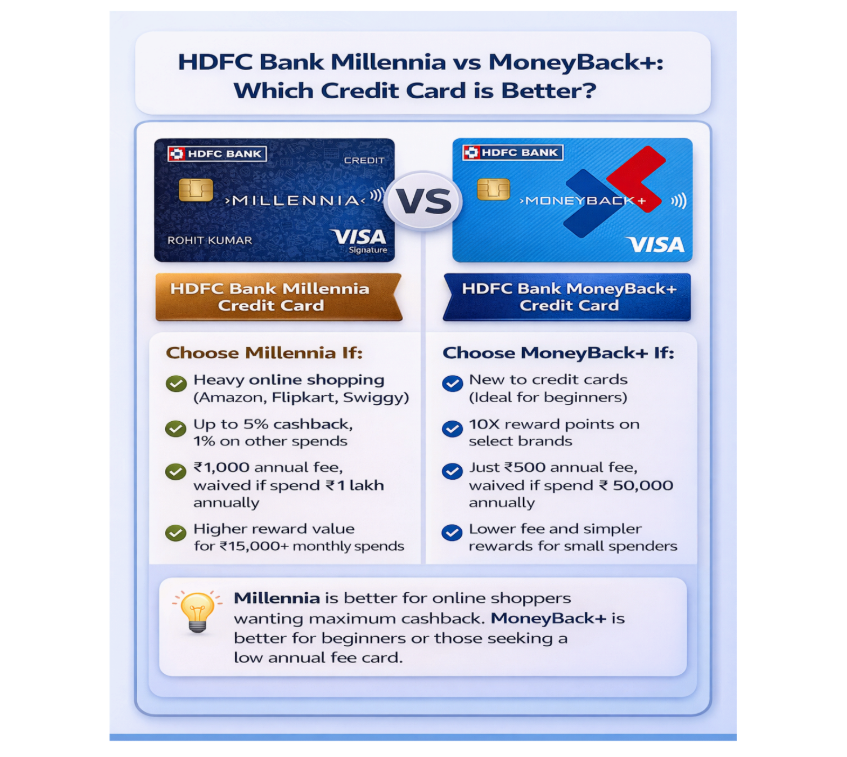

At a high level, the HDFC Bank Millennia Credit Card is designed for heavy online shoppers who regularly use brands like Amazon, Flipkart, Swiggy, Zomato, Myntra, Uber and more. In contrast, the HDFC Bank MoneyBack+ Credit Card targets beginners and low-to-moderate spenders who want a lower annual fee and simple entry into HDFC’s rewards ecosystem.

- Annual/Joining Fee:

- Millennia: ₹1,000 + taxes, with renewal fee waived on annual spends of ₹1,00,000 or more.

- MoneyBack+: ₹500 + taxes, with renewal fee waived on annual spends of ₹50,000 or more.

- Welcome Benefits:

- Millennia: Typically 1,000 CashPoints on payment of joining fee (value depends on redemption mode).

- MoneyBack+: 500 CashPoints on payment of the joining fee.

- Core Rewards Proposition:

- Millennia: Up to 5% cashback on popular brands: Amazon, BookMyShow, Flipkart, Uber, Zomato, Swiggy, Tata CLiQ, Cult.fit, Myntra, and Sony LIV; 1% on other spends.

- MoneyBack+: 10X CashPoints (worth about 3.3% valueback) on a smaller partner set like Amazon, Flipkart, Swiggy, BigBasket, Reliance Smart SuperStore; 2X on other spends.

HDFC Credit Card Rewards Comparison

This is where most people get confused. Both cards give CashPoints, but they work differently.

Cashback vs Reward Points: How They Really Work

Despite being called a "cashback" card, the Millennia actually gives you CashPoints that you need to redeem. The MoneyBack+ is called a "rewards" card, but also gives CashPoints.

The key difference is redemption value:

HDFC Millennia: 1 CashPoint = ₹1 when redeemed against your credit card bill

HDFC MoneyBack+: 1 CashPoint = ₹0.25 when redeemed as cashback This makes a huge difference in actual value.

Real-Life Spending Example

Let's say ₹20,000 monthly is spent on online shopping (Amazon, Flipkart, Swiggy).

With HDFC Millennia:

-

₹20,000 × 5% = 1,000 CashPoints

-

Redemption value: 1,000 × ₹1 = ₹1,000 back

-

Effective return: 5% With HDFC MoneyBack+:

-

₹20,000 spend = ₹18,750 on 5 partner brands (max limit for 10X) + ₹1,250 on 2X

-

10X on ₹18,750: 2,500 CashPoints (monthly cap reached)

-

2X on ₹1,250: Approximately 17 CashPoints

-

Total: 2,517 CashPoints

-

Redemption value: 2,517 × ₹0.25 = ₹629 back

-

Effective return: 3.14%

HDFC Millennia gives 59% more value (₹1,000 vs ₹629).

Apply for a Credit Card & Get Instant Approval

Effective Reward Rate Comparison

Ease of Redemption

Millennia: Redeem directly against your credit card statement at a 1:1 ratio (easiest option)

MoneyBack+: Can redeem as cashback at ₹0.25 per point or convert to shopping vouchers for slightly better value

The Millennia's 1:1 redemption makes it simpler and more valuable for most users.

Detailed Comparison: Millennia vs MoneyBack+

Fees & Charges Comparison

Both cards have similar fee structures:

Joining/Annual Fee:

-

Millennia: ₹1,000 + GST

-

MoneyBack+: ₹500 + GST

Interest Rate on Unpaid Balance:

Late Payment Fee:

Fuel Surcharge Waiver:

-

Millennia: 1% on ₹400-₹4,000 transactions

-

MoneyBack+: 1% on ₹400-₹5,000 transactions (capped at ₹250/month)

Foreign Transaction Fee:

Eligibility Criteria

Both are entry-level HDFC credit cards with easy eligibility requirements:

Age: 21 to 60 years (salaried), 21 to 65 years (self-employed)

Income Requirement:

-

Millennia: ₹25,000 per month for salaried individuals

-

MoneyBack+: ₹25,000 per month for salaried individuals

Documents Required:

-

Identity proof (Aadhaar, PAN card)

-

Address proof (utility bills, rental agreement)

-

Income proof (salary slips for the last 3 months, bank statements)

Credit Score: Generally 750 or above increases approval chances

Apply for a Credit Card & Get Instant Approval

Which Card is Better?

Choosing the right and best HDFC credit card for beginners depends on your spending patterns and financial goals.

Choose HDFC Millennia If:

You're a heavy online shopper: If you regularly spend ₹15,000 or more monthly on Amazon, Flipkart, Swiggy, Zomato, or other partner brands, the 5% cashback (with 1:1 redemption) gives maximum returns.

You want simple cashback: The 1:1 redemption ratio means you don't need to calculate complex point values. What you see is what you get.

You can justify the higher fee: The ₹1,000 annual fee is worth it if you're earning ₹1,000+ in cashback monthly.

You want more brand options: With 10 partner brands instead of 5, you have more flexibility in where you shop.

Example: If ₹18,000 monthly is spent across Amazon (₹8,000), Swiggy (₹4,000), Flipkart (₹3,000), and Uber (₹3,000). Then, 900 CashPoints monthly (₹900) and ₹10,800 annually are earned. After deducting the ₹1,000 annual fee, the net benefit is ₹9,800.

Choose HDFC MoneyBack+ If:

You're new to credit cards: The lower ₹500 annual fee makes it easier to start building your credit history without a big commitment.

Your monthly spending is moderate: If you spend ₹5,000-₹10,000 monthly, the lower fee waiver requirement (₹50,000/year vs ₹1,00,000/year) is more achievable.

You prefer a low-commitment card: Getting your annual fee waived requires half the spending compared to Millennia.

You shop mainly at 5 core brands: If your spending is concentrated at Amazon, Flipkart, BigBasket, Swiggy, and Reliance, you'll still get good value.

Example: If ₹8,000 monthly (₹5,000 on partner brands, ₹3,000 elsewhere) is spent.Then, approximately 430 CashPoints monthly (₹107 after redemption) and totalling ₹1,284 annually are earned. After the ₹500 annual fee, the net benefit is ₹784.

Conclusion: HDFC Bank Millennia vs HDFC Bank MoneyBack+

If your goal is maximum cashback from online shopping, the HDFC Bank Millennia Credit Card generally offers higher effective rewards and stronger HDFC Millennia benefits. If you’re a beginner who values lower fees, simpler approval and decent partner rewards, HDFC Bank MoneyBack+ Credit Card is a practical, low-risk starting point.

In short, Millennia is the value-maximiser, while MoneyBack+ is the starter-friendly option; pick based on your monthly spends and comfort with fees.